With his Showtime Rotisserie, Ron Popeil told us to “Set it and forget it.”

There’s value in setting something up and being able to go about your day, knowing you’ll get an expected result.

Personal finance is more complicated than a rotisserie chicken, there’s wisdom and value in removing as much of that complexity and simplifying as much of it as we can.

The more we can automate our finances, the better our chances of creating a simple path to wealth.

Here’s what we’ll cover:

Let’s get started.

Getting clear on your plan

Obvious? Yes. But the vast majority of people don’t have a clear plan for their finances.

Now, this isn’t a game of perfect, but you do need to get clarity on your desired result. As you go through this process, make sure you know your priorities, and you know how much you want to end up with so you know how much you need to be saving and investing.

Here are some examples:

-

Perhaps you have a retirement goal of $500,000, so you need to be contributing $1,000 a month to your 401(k).

-

Perhaps you have a downpayment goal of $100,000, so you need to be contributing $750 a month to your taxable brokerage account.

-

Perhaps you have an accumulation goal of $40,000 for your kid’s college fund, so you need to be contributing $200 a month to a 529 plan.

-

Perhaps you have an accumulation goal of $2,000 for your annual vacation fund, so you need to be saving $166 a month to a savings account.

Opening required accounts

Once you know your priorities and how much you need to contribute, it’s time to open the required accounts.

If you have a 401(k) at work, get enrolled.

If you’re going to open an IRA, select a custodian and account type (Roth or Traditional), and open your account (M1 Finance is one of our Certified Partners).

For non-qualified, taxable brokerage accounts, select a custodian and open your account (again, M1 Finance).

Make sure your bank allows you to open multiple accounts without additional charges. For each of your financial priorities (vacation fund, emergency fund, etc), you should have a separate account you can transfer money into.

Calendaring your meetings

When you want to ensure something gets done, put it on your calendar.

If I don’t schedule an important meeting, thinking it will simply happen on it’s own, I have a tendency to procrastinate. This commonly happens with personal and family things.

It’s smart to schedule recurring meetings for your personal finances. For example, when you’re getting started with budgeting, schedule a monthly meeting to review your cash flow and budget. This will help you develop a habit, and you’ll get better every time you do it.

I really want to emphasize the importance of scheduling and honoring these meeting times. While we can automate a lot of our finances, we still need to make sure we’re keeping an eye on our cash flow and our budgets.

Taking your hands off the wheel

The more things which can be set to happen without me having to do them, the better.

There are aspects to our financial lives, such as monitoring our spending and cash flow, which we cannot delegate or automate. For activities like bill-paying, monthly contributions and rebalancing, we can most certainly automate.

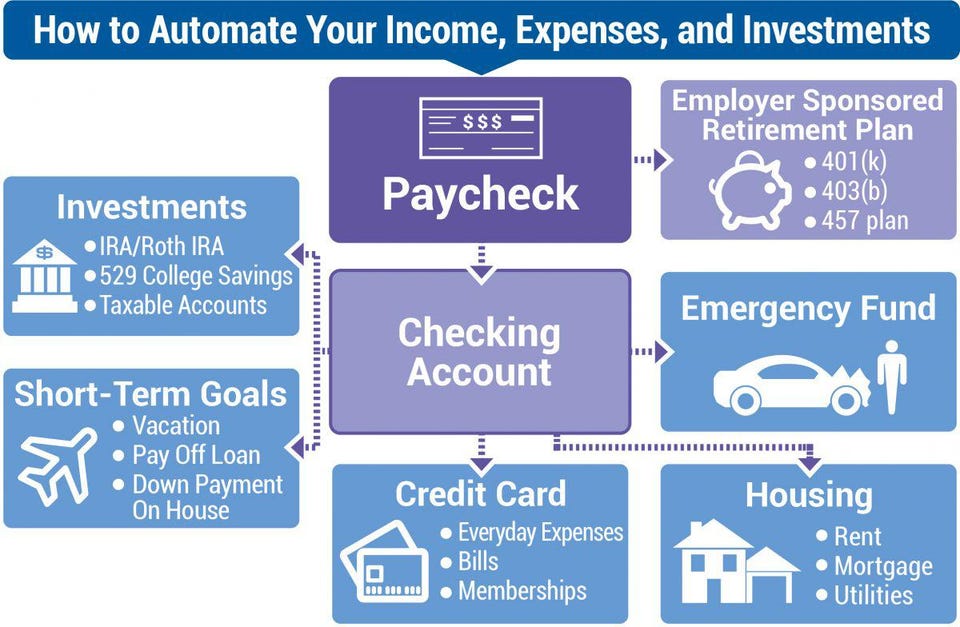

Here’s a helpful visual from Forbes:

Step one: Turn on automatic contributions to your employer-sponsored retirement plan. If possible, also turn on auto-escalate so your deferral percentage increases each year.

Step two: Set up auto-contributions from your checking account to your emergency fund account.

Step three: Set up auto-contributions from your checking account to your taxable brokerage account, college savings account, and any other accounts like an IRA.

Step four: Set up auto-contributions from your checking account to your vacation fund or other saving priorities like a down payment fund.

Step five: Set up auto-contributions from your checking account for all possible bill payments.

Step six: Set up auto-contributions from your checking account to your credit cards.

Consolidating as much as possible

This is a simple step intended to create greater peace of mind. If possible, arrange for all of your bills to come out on the same day(s) each month, such as the 1st or 15th.

I prefer this to seeing deductions on a lot of days throughout the month. Simply personal preference.

For any bills which you cannot set up auto-payment, put due-date reminders into your calendar so you don’t miss any payments.

Implementing technology

I (we) have an interesting relationship with technology. A lot of the time, a new app or program sounds good in theory, but doesn’t add value in practice.

There’s an ever-growing number of apps and fintech companies in the personal finance space, but that doesn’t mean you should adopt or use them. If you have something you like and it works for you, great! If you prefer a less tech-enabled approach to managing your money, that’s great too.

The best way to manage your finances is the way that works for you. I’m fond of saying that I’d rather be useful than brilliant. And just because an app is brilliant, doesn’t mean it will be useful to you.

A word on investing

I am a proponent of a recent innovation known as the robo-advisor. As it sounds, the idea is to combine technology with financial advice. These new platforms utilize the best that algorithms have to offer to make investing better and less expensive.

There are many robo-advisors that specialize in most every type of investing. They can be found in taxable brokerage accounts, as well as qualified plans like IRAs. Along with sophisticated asset allocation models and investment decisions, they also consistently rebalance your portfolio so you don’t need to worry about doing it manually. M1 Finance has a robo-advisor in it’s accounts.

I’m also a fan of target date funds in retirement plans and education funds. These time-based investments make it easy on investors who are not interested in manually making asset allocation decisions, and who are not interested in rebalancing their portfolios every year.

Conclusion

There are a lot of opportunities to “set it and forget it” with our finances. I know I take advantage of as much automation as I can, but I’m not a big user of personal finance apps.

Bottom line is this: find what works and stick to it.

If you’re ready to take control of your financial life, check out our DIY Financial Plan course.

We’ve got three free courses as well: Our Goals Course, Values Course, and our Get Out of Debt course.

Connect with one of our Certified Partners to get any question answered.

Stay up to date by getting our monthly updates.

Check out the LifeBlood podcast.

If you’d like help getting on the same page with your partner, check out our Same $ Page Course.

If you’d like to help your kids get good with money, check out our Teaching Kids about Money course.

LifeBlood is supported by our audience. If you purchase through links on our site, we may earn an affiliate commission. Learn more.