While it may not be possible to completely remove all risk from your financial life, there are a lot of things you can do to position yourself for success.

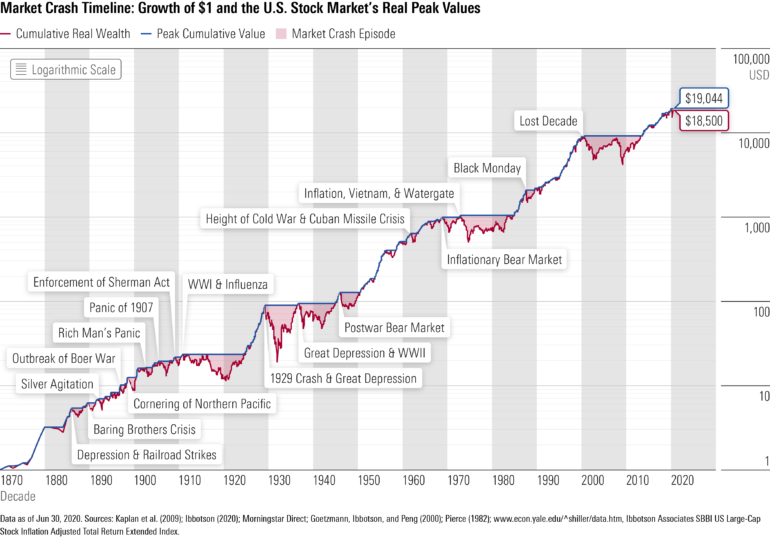

Nobody knows if the stock market will go up or down tomorrow. From 1951 to 2021, the stock market was up 53.7% of the time, and down 46.3% of the time. While that’s close to a 50-50 split, you can see from the chart below that it’s gone up over time.

That chart also shows us that there have been 17 crashes over the past 150 years, characterized by declines of 20% or more.

If a market crash happens when you’re 25 years old, and you’re planning to retire at 65, it’s ok. If you’re 63 and you’ve got two years before retirement, you could be in trouble.

My goal here is to assist you in preparing for your retirement. To help you keep as many variables in perspective as possible, and to position you for success whether the stock market is going up, or it’s going down. Because it’s going to do both of those things.

As a financial advisor, I’ve been helping people to do this for 20+ years. I’m honored to be named to Investopedia’s list of the top 100 financial advisors many years running.

Here’s what we’ll cover:

Guaranteed retirement income

Liquidity needs

Inflation fears

Let’s get started.

Guaranteed retirement income

We all want financial peace of mind. I don’t know anyone who’s interested in worrying about money, particularly during retirement. The antidote to market crashes, and the key to peace of mind is guaranteed retirement income.

Commonly, we get guaranteed income streams from three sources; Social Security, pensions, and annuities. I’m going to go through each of these individually, but when designing retirement income, a good rule of thumb is to have enough guaranteed income to cover your fixed expenses in retirement.

In order to know if you’ll have enough guaranteed income to cover your fixed expenses, you need to know what your fixed expenses will be. Don’t assume they’re going to be the same as what they are today. It’s very possible they’re going to be different. With that in mind, you should create a retirement budget.

Social Security

Do you know what your Social Security benefit will be? You can go to SSA.Gov, create a profile, and get information specific to you.

Social security certainly qualifies as guaranteed retirement income. It will be there for as long as you’re alive, barring absolute catastrophe.

Pensions

It used to be that we’d work at the same company for 30 years, and retire with a gold watch and a lifetime pension. Today, fewer and fewer of us will experience that. If you’re one of the lucky ones, you need to pay close attention to how your pension will work.

You’ll have several payout options which include single life, joint life, and lump sum. When deciding, take all of your other assets into consideration. A pension can be a great source of guaranteed retirement income.

Annuities

Should you Google “annuities,” you’ll probably get results similar to the historical performance of the stock market; half good, and half bad. The reality is, annuities are neither good nor bad. They just are. The key is to determine whether or not they fit into your retirement income picture.

If you are considering an annuity, be sure you understand how the product works. Some annuities are very simple and straightforward, while others are very complex. While I’m a fan of simplicity, that’s just me.

You must also ask about total fees and expenses of these products. If, after everything has been explained, it still doesn’t make sense to you, I would treat that as a red flag. When I encounter financial red flags, I remove myself from the situation and don’t do business with the person or company.

If having enough guaranteed retirement income to cover your fixed expenses makes sense to you, using an annuity to cover any shortfall could be a great option that provides you peace of mind, and a crash proof retirement.

The drawback for this security is a lack of liquidity, and the danger of inflation.

Liquidity needs

Liquidity needs must be taken into consideration in retirement. Just as in your pre retirement life, you need a fully funded emergency fund during retirement. This is particularly true if you’re not going to be working during retirement (therefore not earning additional income).

I’m an advocate for having six month’s worth of expenses as an emergency fund. That doesn’t make it right for you. It’s something you’ll need to decide on yourself. This is another reason for getting clear on your retirement budget.

When you decide what the appropriate amount is for you and your family, resist the impulse to invest that money. Your emergency fund should be in cash in an account that is separate from your everyday checking account.

Inflation fears

I hope you live a long and healthy life. Odds are, you’ll live well into your 80s and 90s. While that’s a positive thing in most ways, it also puts you at risk should inflation be high.

Therefore, consider having a portion of your portfolio in an investment that can keep pace with inflation. This doesn’t mean you should be investing in individual stocks. There are many ways for you to take a moderate approach to investing that can position you for success should inflation be high.

Closing

As you’re designing your retirement income picture, taking guarantees, liquidity, and inflation into consideration is a best-practice. While there’s no way to completely remove market risk, following the steps I’ve laid out can help you crash proof your retirement.

A quick dose of perspective: When you’re in your accumulation years, saving and investing for retirement, you’d rather have the stock market perform poorly. The only time you’d want the market to go up is the day you intend to sell your investments.

Think about it like this; would you rather buy shares of Amazon at $1 a share, or $1,000 a share? Obviously you’d rather buy them at a $1.

If you could buy Amazon for $1 for the next 30 years, and on the day you intended the sell, the price jumped to $1,000, you’d be one happy investor.

It’s really hard to time the market. The best approach is to create your saving and investing plan and to stick to it.

If you’re ready to take control of your financial life, check out our DIY Financial Plan course.

We’re here to help others get better so they can live freely without regret Believing we’ve each got one life, it’s better to live it well and the time to start is now If you’re someone who believes change begins with you, you’re one of us We’re working to inspire action, enable completion, knowing that, as Thoreau so perfectly put it “There are a thousand hacking at the branches of evil to one who is striking at the root.” Let us help you invest in yourself and bring it all together.

Feed your life-long learner by enrolling in one of our courses.

Invest in yourself and bring it all together by working with one of our coaches.

Save that Money: How to Get On The Path to Financial Success Can you remember the first person to tell you, “Save that money?” Was it a parent? Maybe a [...]